Should We Invest in PRS for Tax Reliefs?

For this week’s topic, let us evaluate whether we should be investing in Private Retirement Schemes (PRS) to maximise that RM3,000 tax relief.

This one is more subjective than just ‘don’t go out of your way to spend’, because saving for retirement is supposed to be good. So why not get tax relief along the way?

Let us consider PRS now as an investment. There are two components that contribute to the total return of PRS, namely the fund returns itself PLUS the value of tax savings. This is in contrast to most investments, including a similar investment type called Unit Trust, where the total returns depend entirely on the fund returns.

Now in essence, the decision to invest in PRS comes down to whether its total expected return is more than or less than another investment. For example, say the total return of PRS, including tax relief, is 5% per year. Then any investment that does more than 5% should be better, assuming other factors like risk are roughly similar.

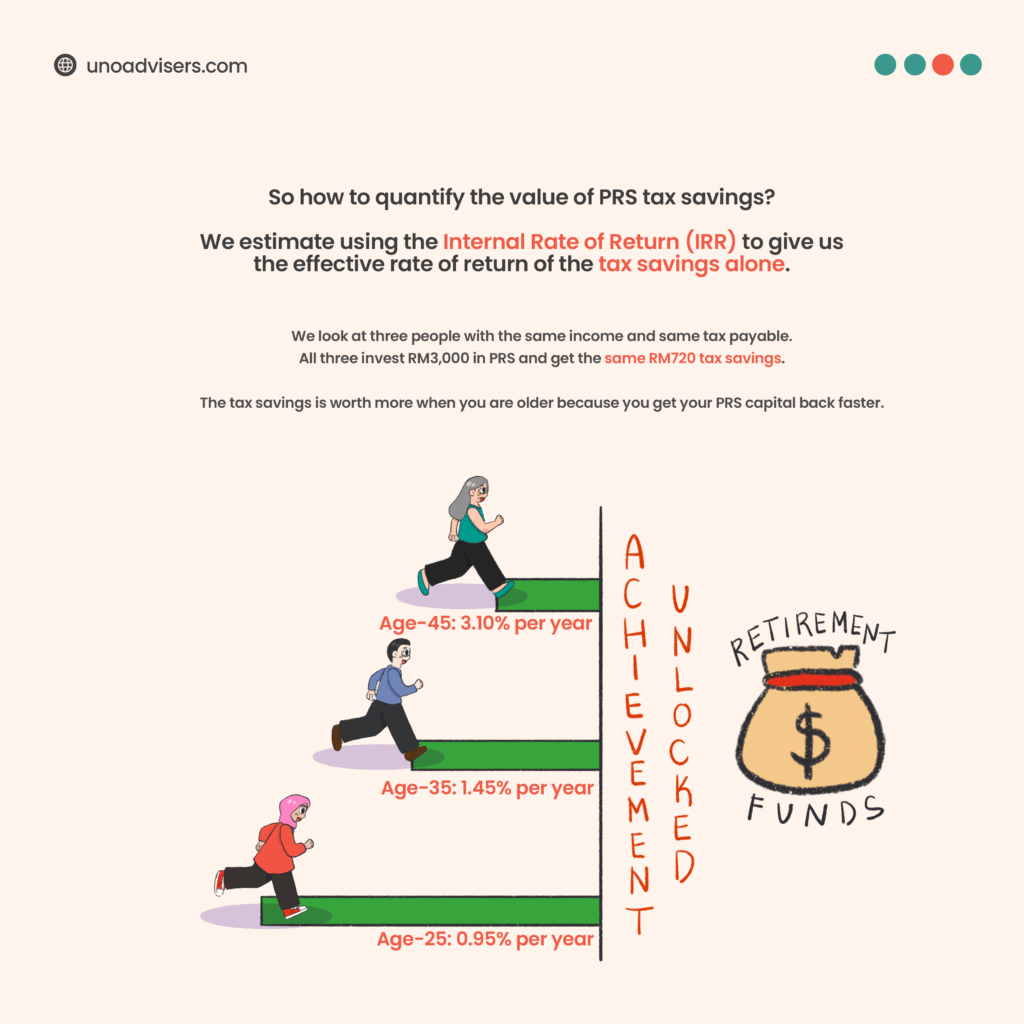

As you may be already wondering though, how do you factor in tax relief into the annual return percentage? It is not entirely straightforward to turn a one-time, flat number tax savings into an annual percentage return. So to quantify it, let’s use the Internal Rate of Return (IRR) to estimate the effective annual return of just the tax savings alone. IRR is a financial metric used to evaluate investments of different types, so that it is easier to compare. In this case we will use the IRR as the estimated annual rate of return of the tax relief.

Let’s look at three people of different ages: age-25, age-35, and age-45. We assume they all earn RM10,000 monthly, have income clearly in the 24% tax bracket, and will all retire at age-55. They all put RM3,000 into PRS which can only be withdrawn at age-55. Also note that generally speaking, the faster you get your capital back, the better.

All three people will save the same amount of tax because they are at the same income level. The total tax saved is a one-time RM720. However each of them has a different time length before getting their capital back (age-25 person requiring the longest time).

Factoring in the different time lengths, we get the following IRR values of the one-time RM720 savings:

Age-25 : 0.95% per year

Age-35: 1.45% per year

Age-45: 3.10% per year

That is to say the one time RM720 savings is equivalent to 0.95% return per year on the age-25 person’s RM3,000 PRS investment. The same RM720 tax savings is worth more to the age-35 and age-45 people generally because as mentioned earlier, they get their RM3,000 capital back faster.

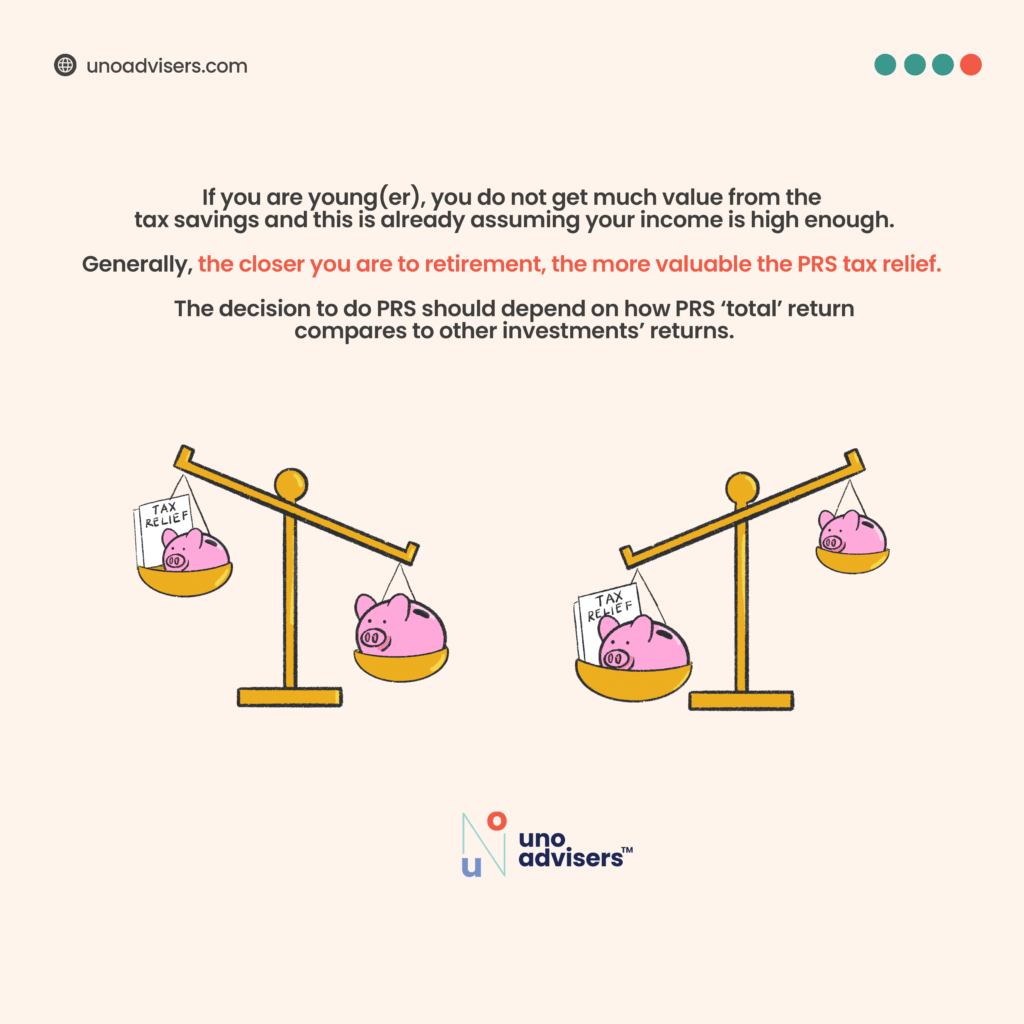

The key takeaway is that if you are young, PRS tax relief may not be giving you that much benefit and many investments will outperform it. However, the closer you are to retirement, the more valuable the tax relief will be.